Net Worth by Age 2026: US Median Benchmarks (Federal Reserve Data)

Income determines how much money enters your life. Net worth determines how much stays.

That distinction matters because the two are not as correlated as most people assume. A household earning $200,000 per year with a $1.2 million mortgage, two car loans, and no retirement savings has a lower net worth than a household earning $80,000 that has been investing steadily for 20 years. The income number looks better. The net worth number tells the real story.

Most people track their income carefully and their net worth almost not at all. This guide gives you the real benchmarks -- actual median figures from the Federal Reserve's 2022 Survey of Consumer Finances, the most authoritative source of US household wealth data available -- so you can see where you actually stand.

Key Takeaways

- ✓Median net worth is usually more useful than average net worth because it is not distorted by extreme wealth at the top of the distribution

- ✓The Federal Reserve's 2022 Survey of Consumer Finances (SCF) is the most current authoritative source of US household wealth data; the next update is expected in late 2026

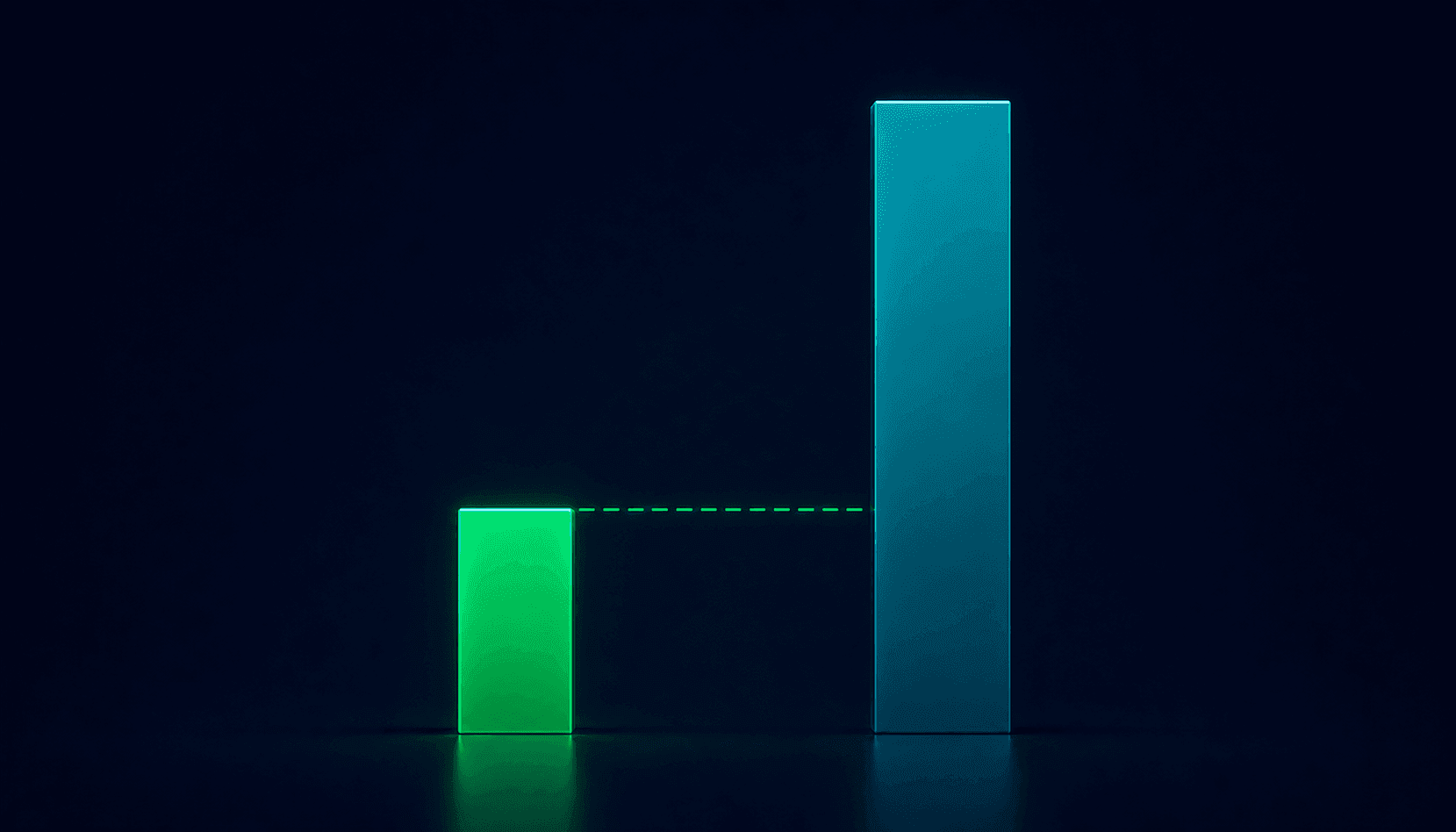

- ✓Overall US median household net worth in 2022 was $192,700; the average was $1,063,700 -- a gap that illustrates how concentrated wealth is at the top

- ✓Median net worth peaks between ages 65-74 at $409,900, then declines as retirees draw down savings

- ✓Under-35 households had a median net worth of $39,000 in 2022, up dramatically from $13,900 in 2019 due to rising home prices and stock market gains

- ✓Home equity makes up the majority of net worth for middle-wealth households; excluding it drops the overall median from $192,700 to roughly $57,900

- ✓High income does not guarantee high net worth; lifestyle inflation and debt are the most common reasons high earners end up below their age-group median

- ✓Negative net worth is common in your 20s and early 30s, particularly with student loan debt; it is a starting point, not a permanent condition

Net Worth Benchmark Summary

| Age | Median Net Worth |

|---|---|

| Under 35 | $39,000 |

| 35-44 | $135,600 |

| 45-54 | $247,200 |

| 55-64 | $364,500 |

| 65-74 | $409,900 |

| 75+ | $335,600 |

Source: Federal Reserve SCF 2022.

On This Page

- 1.Net worth by age: quick answer

- 2.What is net worth?

- 3.Why median matters more than average

- 4.What is a good net worth by age?

- 5.Detailed net worth benchmark table

- 6.Real example 1: 28-year-old employee

- 7.Real example 2: 40-year-old family

- 8.Real example 3: 55-year-old professional

- 9.Why high income does not guarantee high net worth

- 10.How to increase net worth faster

- 11.Net worth vs income

- 12.Net worth vs emergency fund

- 13.Net worth calculator example

- 14.Common net worth mistakes

- 15.One-minute net worth audit

- 16.Quick answers

- 17.Frequently asked questions

Net worth by age: quick answer

Quick Answer

US median net worth ranges from approximately $39,000 for households under 35 to $409,900 for households aged 65-74. These figures are from the Federal Reserve's 2022 Survey of Consumer Finances, the most current authoritative data available.

| Age Group | Median Net Worth | Average Net Worth | Notes |

|---|---|---|---|

| Under 35 | $39,000 | $183,500 | Student loans and limited savings history; average is 4.7x median |

| 35-44 | $135,600 | $549,000 | Mortgage, peak debt years; home equity starts building |

| 45-54 | $247,200 | $975,800 | Peak earning years; retirement accounts growing |

| 55-64 | $364,500 | $1,566,900 | Pre-retirement; largest wealth accumulation decade |

| 65-74 | $409,900 | $1,794,600 | Net worth peaks; Social Security begins |

| 75+ | $335,600 | $1,624,100 | Drawdown phase; spending savings in retirement |

| All households | $192,700 | $1,063,700 |

Source: Federal Reserve Board, 2022 Survey of Consumer Finances (SCF), published October 2023. The 2025 SCF is currently being conducted with results expected late 2026.

Why median, not average:

The average US household net worth of $1,063,700 is technically accurate but practically misleading. It is pulled upward by a small number of extraordinarily wealthy households. A community of 10 people where nine have $100,000 and one has $10 million has an “average” net worth of just over $1 million -- but nine out of ten people are far below that. The median ($100,000 in that example) tells you what the typical person actually has. For personal benchmarking, the median is almost always the more useful number.

What is net worth?

Direct Answer

Net worth is the total value of everything you own minus everything you owe.

Assets minus liabilities equals net worth.

Net Worth = Total Assets - Total LiabilitiesAssets include

- +Cash and bank account balances

- +Retirement accounts (401k, IRA, pension value)

- +Investment accounts (brokerage, index funds)

- +Primary home market value

- +Other real estate

- +Vehicle value

- +Business ownership value

- +Other valuable property

Liabilities include

- -Mortgage balance

- -Car loans

- -Student loans

- -Credit card balances

- -Personal loans

- -Medical debt

- -Any other money owed

Simple example:

A 38-year-old with a home worth $350,000 (mortgage balance $240,000), a 401k worth $85,000, $15,000 in savings, and $22,000 in student loans:

Total assets: $350,000 + $85,000 + $15,000 = $450,000

Total liabilities: $240,000 + $22,000 = $262,000

Net worth: $450,000 - $262,000 = $188,000

That $188,000 is above the 35-44 median of $135,600. It does not feel wealthy, but it is ahead of the typical household in that age group.

Net worth is a stock, not a flow. Your paycheck is a flow -- money moving through your life. Net worth is what accumulates after that flow. Two households can have identical incomes and very different net worths depending on spending, debt, and investment habits.

Why median net worth matters more than average

Direct Answer

The median is the value at the exact middle of the distribution. Half of households have more, half have less. The average is pulled dramatically upward by extreme wealth at the top, making it almost useless as a personal benchmark.

Consider the 55-64 age group. The median net worth is $364,500. The average is $1,566,900. If you compare yourself to the average and you have $400,000, you feel behind. But $400,000 in that age group actually puts you above the median -- you have more than half of American households in your cohort. The average made you feel like a failure when you are actually doing better than most.

| Age Group | Median | Average | Average / Median Ratio |

|---|---|---|---|

| Under 35 | $39,000 | $183,500 | 4.7x |

| 35-44 | $135,600 | $549,000 | 4.0x |

| 45-54 | $247,200 | $975,800 | 3.9x |

| 55-64 | $364,500 | $1,566,900 | 4.3x |

| 65-74 | $409,900 | $1,794,600 | 4.4x |

Source: Federal Reserve SCF 2022.

The pattern is consistent: across every age group, the average is roughly 4-5x the median. This ratio exists because a small fraction of households hold an outsized share of total wealth. The top 1% of US households holds approximately 30% of all household wealth according to Federal Reserve Distributional Financial Accounts.

When financial media says “the average American has X in retirement savings,” they often mean the mean, not the median. The median figure is usually 50-70% lower. Both numbers are accurate. Only one is useful for comparing where a typical person stands.

What is a good net worth by age?

Direct Answer

A “good” net worth depends on your definition of good. At the median, you are ahead of half of Americans in your age group. At the 75th percentile, you are ahead of three-quarters. At the 90th percentile, you are in the top 10%.

The practical framework:

| Level | Definition | Meaning |

|---|---|---|

| Below median | Less than half of households your age | Common, especially in 20s and 30s; focus is on building |

| At median | 50th percentile for your age group | Typical American household |

| Above median (25-50% ahead) | 60th-70th percentile | Ahead of the typical household; progressing well |

| Top 25% (75th percentile) | 25% of households have more | Meaningfully ahead; on track for financial security |

| Top 10% (90th percentile) | 10% of households have more | High wealth relative to peers |

Important context: Being at or below the median at 28 is completely normal. Student loans, entry-level income, and limited time to save all create early-career net worth deficits that are entirely expected. Net worth below median in your 30s is also common for people who bought homes in expensive markets and carry significant mortgage debt. The trajectory matters as much as the current number.

Detailed net worth benchmark table

The following table shows median net worth alongside 75th percentile and 90th percentile thresholds, all from the Federal Reserve SCF 2022 data and supplemental analysis from DQYDJ and Federal Reserve Distributional Financial Accounts.

| Age Group | Median (50th %ile) | 75th Percentile | 90th Percentile | Average |

|---|---|---|---|---|

| Under 35 | $39,000 | ~$150,000 | ~$390,000 | $183,500 |

| 35-44 | $135,600 | ~$470,000 | ~$980,000 | $549,000 |

| 45-54 | $247,200 | ~$780,000 | ~$1,760,000 | $975,800 |

| 55-64 | $364,500 | ~$1,100,000 | ~$2,600,000 | $1,566,900 |

| 65-74 | $409,900 | ~$1,200,000 | ~$3,200,000 | $1,794,600 |

| 75+ | $335,600 | ~$900,000 | ~$2,750,000 | $1,624,100 |

Source: Median figures from Federal Reserve SCF 2022 (published October 2023). Percentile figures derived from SCF microdata analysis by DQYDJ and Federal Reserve Distributional Financial Accounts. All figures approximate.

The under-35 median jumped from $13,900 in 2019 to $39,000 in 2022 -- the largest jump for any age group. This was driven by rising home prices and stock market gains between 2019 and 2022. The 2025 SCF results (expected late 2026) may show different trends depending on market conditions since 2022.

Net worth peaks at ages 65-74 at $409,900, then drops to $335,600 at 75+. This reflects the drawdown phase: retirees spending down savings and drawing Social Security. It is not a sign of financial distress for most households; it is the natural pattern of retirement spending.

The jump from median to 75th percentile is large: roughly 3-4x across most age groups. This reflects wealth concentration even within the 'ahead of average' tier.

Real example 1: 28-year-old employee

Profile: Marketing coordinator, $52,000/year salary, rents an apartment, has student loans.

Assets

Liabilities

Net worth: $27,600 - $35,700 = -$8,100

Benchmark comparison: Under-35 median is $39,000. This person is below the median. But they are 28, have $12,400 in retirement savings, and their student loans are manageable relative to income. Negative net worth at 28 is common and not alarming when it is primarily student debt with a clear payoff path.

The realistic trajectory: If this person contributes $200/month to their 401k, pays an extra $200/month on student loans, and avoids new consumer debt, they are likely to reach positive net worth by 30-31 and the under-35 median by 33-34.

Real example 2: 40-year-old family

Profile: Dual-income household, two children. Combined income $130,000. Homeowners, both have 401ks.

Assets

Liabilities

Net worth: $575,000 - $325,500 = $249,500

Benchmark comparison: The 35-44 median is $135,600. This household is at approximately the 65th-70th percentile for their age group -- ahead of most households in their cohort. The home equity ($90,000) and retirement savings ($145,000) are doing the heavy lifting.

What this household should watch: Lifestyle inflation as income grows, keeping car loans small, and continuing retirement contributions even as expenses increase with children.

Real example 3: 55-year-old professional

Profile: Senior engineer, $145,000 salary, married, adult children, owns home free and clear, maxed retirement accounts for 15 years.

Assets

Liabilities

Net worth: $1,570,000 - $9,700 = $1,560,300

Benchmark comparison: The 55-64 median is $364,500. This household is comfortably in the top 25% for their age group, likely near the 90th percentile. The combination of a paid-off home and 25+ years of consistent retirement contributions drives the result.

The takeaway from this example: Net worth at this level is almost entirely the result of consistent behavior over 25 years, not a single windfall. The math of compounding means early contributions in the 30s created most of the value. Starting late is not catastrophic, but starting early is substantially better.

Why high income does not guarantee high net worth

Direct Answer

Income determines what could accumulate. Net worth reflects what did accumulate. Lifestyle inflation, debt, and consumption convert high income into high spending without building lasting wealth.

This is the personal finance pattern that surprises people most. A household earning $250,000 with a $1.5 million mortgage, two luxury car leases, private school tuition, frequent travel, and no retirement savings can have a lower net worth than a household earning $90,000 that has been investing 15% of income consistently.

The mechanics:

Income is a flow. It comes in and goes out. Net worth is a stock. It either accumulates or it does not, depending on what happens to the flow.

Three specific behaviors convert high income into low net worth:

Lifestyle inflation

Every income increase gets consumed by proportionally higher spending. New car, bigger house, more travel, more subscriptions. Income goes up 20%, spending goes up 18%, savings rate barely changes.

Debt that funds lifestyle

A $600,000 mortgage, $70,000 in car loans, and $30,000 in consumer debt does not reduce income -- it reduces net worth. The assets purchased may appreciate (the home) or depreciate (the car), but the liability is real immediately.

Delayed investing

A 35-year-old making $180,000 who has not started seriously investing has a lower net worth than a 35-year-old making $70,000 who has contributed to a 401k for 10 years. Income history matters less than when you started accumulating.

An actual example:

Household A -- $220,000 income

- $1.8M home (mortgage $1.4M)

- Two $60,000 cars (leased)

- No retirement savings

- $15,000 credit card balance

Net worth: ~$385,000

Household B -- $85,000 income

- $280,000 home (mortgage $140,000)

- Modest car (owned)

- $210,000 in retirement accounts

- $8,000 savings

Net worth: ~$358,000

How to increase net worth faster

Net worth grows through two levers: increasing assets or decreasing liabilities. The fastest progress typically comes from attacking both simultaneously.

Build a starter emergency fund first

$1,000-$2,000 before aggressive debt payoff. Prevents new debt from disrupting progress. See the Emergency Fund Calculator guide for how much you need.

Reduce high-rate debt

Credit card debt at 20-29% is destroying net worth faster than most investments can rebuild it. Paying off a $5,000 balance at 24% APR is a guaranteed 24% return on that $5,000. Use a systematic payoff approach; see the Debt Snowball vs Avalanche guide for the comparison.

Invest consistently, starting now

Time in the market compounds; starting at 25 vs starting at 35 can mean 2-3x more wealth by 65. Even modest amounts matter: $200/month at 7% average return from age 25 = approximately $525,000 by 65. The Compound Interest Explained guide shows the math behind this.

Avoid lifestyle inflation on income increases

When income rises, save or invest a significant portion before adjusting lifestyle. The "50% rule": put at least 50% of any income increase toward net worth improvement (debt payoff, investing, or savings) before increasing spending.

Protect your biggest asset

For most households, the home is the largest asset and the mortgage is the largest liability. Buying within your means and building equity creates net worth passively over time. Buying at the edge of affordability with a high loan-to-value ratio creates a fragile balance sheet.

Track regularly

Net worth you do not measure tends to drift. Calculate it quarterly; it takes 15 minutes. The Vortenza Net Worth Calculator can be used to track assets and liabilities over time.

Net worth vs income

| Factor | Income | Net Worth |

|---|---|---|

| What it measures | Money flowing in per period | Accumulated wealth at a point in time |

| Time frame | Monthly, annual | Snapshot (changes over time) |

| Determines | Current spending capacity | Financial security and future options |

| Affected by | Job, hours, market | Spending, debt, investing, time |

| Can be high with other low? | Yes -- high earners with no savings | Yes -- retirees with wealth but no income |

| Primary driver | Career, skills, market | Behavior over time |

| Better for comparing to peers | Misleading without context | More accurate measure of financial position |

Net worth vs emergency fund

Direct Answer

Emergency funds are a component of net worth, but a small and specific one. Net worth is the full picture of financial health. An emergency fund is one asset class within that picture, optimized for a different purpose.

Emergency funds are typically $10,000-$30,000 held in a high-yield savings account. At a 35-44 household level, $20,000 in emergency savings represents about 15% of the median net worth of $135,600.

If you are comparing the two in priority order: build the emergency fund first ($1,000-$2,000 starter), then attack high-rate debt, then build full emergency fund while investing. See the full framework in the Emergency Fund Calculator guide.

Net worth calculator example

Net worth calculation is simple arithmetic once you have the inputs. The formula:

Net Worth = Sum of all assets - Sum of all liabilitiesThe work is gathering the numbers. Most people have 4-8 significant assets and 2-6 significant liabilities. A full calculation for a typical household takes 20-30 minutes once a year, less if you update it quarterly.

What to gather

Assets

- +Bank and savings account balances

- +Retirement account balances (401k, IRA)

- +Investment account balances

- +Home value estimate (Zillow/Redfin)

- +Vehicle values (Kelley Blue Book)

Liabilities

- -Outstanding mortgage balance

- -All loan balances (student, auto, personal)

- -Credit card balances

- -Any other debts

Subtract total liabilities from total assets. Update this number at least annually, and when a major financial change occurs (home purchase, job change, large debt payoff).

Common net worth mistakes

Forgetting to count liabilities

Listing assets without debts significantly overstates net worth. Every loan, every credit card balance, every outstanding obligation reduces net worth. A $350,000 home with a $290,000 mortgage contributes $60,000 to net worth, not $350,000.

Overvaluing assets

Using purchase price instead of current market value for homes and vehicles. A car bought for $35,000 two years ago may be worth $22,000 today. Use current market estimates, not what you paid.

Comparing to averages instead of medians

Average net worth is dramatically higher than median in every age group. Comparing to averages makes most people feel far behind when they are actually near or above typical. Use the median as your primary benchmark.

Ignoring retirement accounts

401k, IRA, and pension values count as assets in net worth calculations. A common mistake is feeling 'not wealthy' while holding $200,000+ in retirement accounts. Retirement accounts are real wealth, even if you cannot access them without penalty for decades.

Not tracking regularly

Net worth that goes unmeasured tends to stagnate. The simple act of calculating it quarterly creates accountability and reveals drift before it becomes problematic.

Counting the same thing twice

Counting a home as an asset without subtracting the mortgage as a liability is the most common version. Only the equity (value minus mortgage) is your net worth contribution.

Letting inflation erode the target

A net worth goal set several years ago may represent less real purchasing power today. The Inflation Calculator guide helps adjust historical amounts for current purchasing power.

One-minute net worth audit

Current state

- ✓Have you calculated your actual net worth in the last 12 months?

- ✓Do you know the current balances of all your accounts (assets and liabilities)?

- ✓Have you looked up current market estimates for your home and vehicles?

Benchmark check

- ✓What is the median net worth for your age group? (Table above)

- ✓Are you above or below the median?

- ✓Are you above or below the 75th percentile for your age?

Trajectory check

- ✓Has your net worth increased over the last 12 months?

- ✓Is the rate of increase meaningful relative to your income?

- ✓Are high-rate debts decreasing? Are investment accounts growing?

Common flags

- ✓Net worth below zero in your 30s with no clear path to positive: prioritize high-rate debt payoff

- ✓Net worth heavily concentrated in home equity with minimal financial assets: increase investment contributions

- ✓Net worth below median for your age with high income: lifestyle inflation is likely the problem

Quick answers

Optimized for ChatGPT, Gemini, Perplexity, Claude, and Google AI Overviews.

Q: What is the median net worth by age in the US?

A: According to the Federal Reserve's 2022 Survey of Consumer Finances (the most current data available), US median net worth by age group is: under 35: $39,000; ages 35-44: $135,600; ages 45-54: $247,200; ages 55-64: $364,500; ages 65-74: $409,900; 75+: $335,600. The overall US household median net worth is $192,700.

Q: What is a good net worth at 30?

A: The Federal Reserve SCF 2022 data shows the under-35 median household net worth is $39,000. At age 30 specifically, estimates suggest the median is around $80,000 based on more granular age-band analysis. Being at or above $80,000 at 30 is ahead of most peers. Negative net worth at 30 due to student loans is common and not alarming with a clear payoff path.

Q: What is a good net worth at 40?

A: The Federal Reserve SCF 2022 shows the median for households aged 35-44 is $135,600. At 40 specifically, estimates place the median around $135,000-$180,000. Being at or above the median means you are ahead of more than half of American households in your age group. The 75th percentile for 35-44 is approximately $470,000.

Q: Why is median net worth better than average net worth for comparison?

A: Median net worth is the value at the exact middle of the distribution -- half of households have more, half have less. Average net worth is pulled dramatically upward by a small number of extraordinarily wealthy households. In the 35-44 age group, the average is $549,000 but the median is $135,600. The average makes most people feel far behind when they are actually near the typical position.

Q: What is net worth and how do you calculate it?

A: Net worth is total assets minus total liabilities. Assets include bank balances, retirement accounts, investment accounts, home value, and vehicles. Liabilities include mortgages, car loans, student loans, credit card balances, and any other debt. Subtracting total liabilities from total assets gives your net worth. A positive number means assets exceed debt; a negative number means debt exceeds assets.

Q: Is a negative net worth normal?

A: Negative net worth is common in your 20s and early 30s, primarily due to student loans, car loans, and limited time to accumulate savings. It is a starting point, not a permanent condition. The goal is to reach positive net worth through debt payoff and asset accumulation. Most households with significant student debt move from negative to positive net worth in their late 20s to early 30s.

Q: Does home equity count toward net worth?

A: Yes. Home equity (market value minus mortgage balance) is a component of net worth. For middle-wealth American households, home equity is the largest single asset. The Federal Reserve data shows that excluding home equity drops the overall median net worth from $192,700 to approximately $57,900. Home equity is real wealth, but it is illiquid -- you cannot spend it without selling or borrowing against the property.

Q: Should retirement accounts count toward net worth?

A: Yes. 401k, IRA, and pension values are assets and count fully toward net worth. Many people underestimate their net worth by forgetting their retirement accounts. A common oversight: feeling 'not wealthy' while holding $180,000 in a 401k that does not feel like accessible money. It is real wealth with deferred tax treatment.

Q: How much net worth should I have at 50?

A: The Federal Reserve SCF 2022 shows the 45-54 age group median is $247,200. At 50 specifically, this figure is a reasonable benchmark. Being above $247,200 at 50 means you are ahead of more than half of US households in your age range. The 75th percentile for 45-54 is approximately $780,000.

Q: What is the average net worth at retirement age?

A: The Federal Reserve SCF 2022 shows the 65-74 age group median net worth is $409,900 and the average is $1,794,600. The gap between median and average reflects wealth concentration. Most households entering retirement at 65-74 have a net worth around $400,000, which includes home equity and retirement savings. Social Security supplements this for most retirees.

Q: How does income affect net worth?

A: Income provides the potential to build net worth, but does not guarantee it. Income determines how much money flows in; behavior (spending, debt management, investing) determines how much stays and accumulates. High-income households with significant debt and high spending can have lower net worth than moderate-income households with consistent investing habits.

Q: What percentage of Americans have a net worth over $1 million?

A: Approximately 10-12% of US households have a net worth over $1 million based on Federal Reserve SCF 2022 data. The threshold to be in the top 10% of US households overall (regardless of age) is approximately $1.94 million.

Q: Is $500,000 net worth good for a 45-year-old?

A: Yes. The Federal Reserve SCF 2022 shows the median for 45-54 is $247,200. $500,000 at 45 is roughly at the 70th-75th percentile for that age group -- ahead of 70-75% of American households in the same age range. The 75th percentile for 45-54 is approximately $780,000, so $500,000 sits between the median and the 75th percentile.

Q: How does net worth change after retirement?

A: Net worth typically peaks at ages 65-74 and then declines. The Federal Reserve SCF shows median net worth falling from $409,900 at 65-74 to $335,600 at 75+. This reflects the drawdown phase: retirees spending savings, taking Social Security, and potentially facing higher healthcare costs. The decline is expected and is not necessarily a sign of financial trouble.

Q: How do I increase my net worth quickly?

A: The fastest levers are: paying down high-rate debt (a guaranteed return equal to the interest rate), increasing investment contributions (particularly in tax-advantaged accounts), and avoiding lifestyle inflation when income increases. 'Quickly' is relative -- most meaningful net worth improvement happens over years, not months. The biggest single decision is usually avoiding high-rate consumer debt.

The Biggest Net Worth Mistake

Most people compare their income to other people.

Financially successful people compare their net worth trajectory to their own previous years.

Frequently asked questions

What is a good net worth at 30?+

The Federal Reserve's 2022 Survey of Consumer Finances places the under-35 household median at $39,000. More granular analysis of the SCF data suggests the median for 30-34 year olds specifically is approximately $80,000-$85,000. At 30, being positive (net worth above zero) with a clear plan to grow is the practical benchmark. Many 30-year-olds carry student loans that create negative or near-zero net worth. That is normal for people who took on significant education debt and recently started careers. The trajectory -- are you adding to net worth or losing ground? -- matters as much as the current number.

What is a good net worth at 40?+

The Federal Reserve SCF 2022 shows the 35-44 age group has a median net worth of $135,600. At 40 specifically, estimates from SCF microdata analysis place the median around $135,000-$180,000. Being at or above this range means you are ahead of more than half of American households in your age group. The 75th percentile for 35-44 is approximately $470,000. A practical target for motivated savers at 40: 2-3x annual income in total net worth, which typically works out to $150,000-$350,000 for middle-income households.

Is negative net worth normal and what should I do about it?+

Negative net worth is common in the 20s and early 30s, particularly among people with student loan debt and limited time to save. The Federal Reserve data shows that a meaningful percentage of under-35 households have negative net worth. It is a starting point, not a permanent condition. The path from negative to positive net worth: stop adding new debt, build a small emergency fund ($1,000-$2,000), then systematically pay down high-rate debt while making minimum payments on lower-rate debt. Most people with manageable student debt relative to income reach positive net worth in their late 20s to early 30s if they focus on it.

Does home equity count in net worth calculations?+

Yes, fully. Home equity (current market value minus remaining mortgage balance) is the largest asset for most middle-wealth American households. If your home is worth $350,000 and your mortgage balance is $240,000, your home contributes $110,000 to your net worth. One important nuance: home equity is illiquid. You cannot spend it without selling the property or taking on debt (HELOC, cash-out refinance). High home equity with limited liquid savings creates a situation where you are technically wealthy but cash-poor. A balanced net worth includes both home equity and liquid financial assets.

Should retirement accounts count in net worth?+

Yes. Retirement accounts (401k, IRA, pension) are assets and count fully in net worth calculations. The funds have restrictions on when they can be accessed penalty-free (typically age 59.5 for most account types), but they are real wealth with real value. A common psychological mistake: undervaluing retirement accounts because they 'do not feel accessible.' If you have $250,000 in a 401k, that is $250,000 in net worth. Including them gives you an accurate picture of your financial position.

Why do high earners sometimes have low net worth?+

Income is a flow -- money moving through your financial life. Net worth is a stock -- what accumulates after the flow. High earners with high spending, significant debt, and delayed investing can have lower net worth than moderate earners with disciplined saving habits. The most common pattern: income increases are matched by proportional lifestyle increases (larger house, nicer cars, more travel) without increasing savings rate. After 15 years of earning $200,000 and spending $190,000, the net worth is lower than it would have been on $90,000 with a 20% savings rate.

How often should I calculate my net worth?+

Once per quarter is a reasonable cadence for most people. Annual at minimum. The value of tracking net worth is that it shows drift before it becomes a crisis -- if net worth is declining or stagnating in your 40s and 50s, that is useful information when there is time to correct it. Monthly tracking is helpful during periods of active debt payoff or aggressive saving. The calculation takes 15-30 minutes with organized records.

What is the difference between net worth and wealth?+

Technically, net worth and wealth describe the same thing: the difference between what you own and what you owe. In common usage, 'wealth' often implies a higher level of net worth or a qualitative judgment about financial abundance. From a data perspective, the Federal Reserve SCF uses net worth as the primary measure. For practical purposes, your net worth is your wealth. The word choice does not change the underlying calculation.

How does student loan debt affect net worth in your 20s?+

Student loan debt directly reduces net worth by the outstanding balance. A 25-year-old with $45,000 in student loans has their net worth reduced by $45,000 relative to an equivalent person with no student debt. The counterbalancing factor is that the education financed by those loans theoretically increases earning capacity, which over a career translates to higher savings potential. The net effect of student debt on lifetime net worth depends on the income premium the degree produces versus the debt service cost and time to payoff.

Does the Federal Reserve update net worth data regularly?+

The Federal Reserve conducts the Survey of Consumer Finances every three years. The most recent data is from the 2022 survey, published in October 2023. In February 2025, the Federal Reserve announced the 2025 survey was underway, with results expected in late 2026. The 2022 data is the most authoritative source available through mid-2026.

What is included in the Federal Reserve's net worth calculation?+

The Federal Reserve SCF includes all financial assets (bank accounts, retirement accounts, direct investment holdings, cash value of life insurance) and nonfinancial assets (primary residence, other real estate, vehicles, business equity, valuables) as assets. Liabilities include all forms of debt: mortgage, home equity loans, car loans, student loans, credit cards, and other debts. The resulting calculation (assets minus liabilities) is net worth. The SCF is considered the gold standard for US household wealth measurement because it oversamples wealthy households to ensure accurate top-of-distribution estimates.

What net worth is needed to retire comfortably?+

The widely used rule of thumb is 25x annual spending (based on the 4% safe withdrawal rate). If you plan to spend $60,000/year in retirement, you need approximately $1.5 million in investable assets. If you plan to spend $80,000/year, approximately $2 million. These figures are for investable assets (retirement accounts, brokerage accounts) and typically do not count home equity unless you plan to downsize. The Federal Reserve SCF shows the median 65-74 household net worth is $409,900 -- significantly below the amount needed to fully self-fund retirement, which is why Social Security is critical for most American retirees.

How does inflation affect net worth benchmarks?+

Inflation erodes the purchasing power of a given dollar amount over time. The 2022 SCF benchmarks represent 2022 dollar values. By 2026, inflation has reduced the real value of those amounts by roughly 8-12% cumulatively. When comparing your current net worth to 2022 benchmarks, a rough adjustment is to add 10-12% to the published benchmarks to account for inflation since the data was collected.

Is it better to have high net worth or high income?+

For long-term financial security, net worth matters more. Income is earned each period and can stop. Net worth, once accumulated, generates returns independently of current work. A household with $2 million in investments earning 5% generates $100,000/year passively. A household with $250,000 in annual income but minimal savings generates nothing when income stops. Income is the mechanism for building net worth; net worth is the destination. A high earner who converts income to net worth through investing and debt management achieves both.

How does race and education affect net worth benchmarks?+

The Federal Reserve SCF shows significant disparities in net worth by race and education level. White non-Hispanic households had a 2022 median net worth of $285,000. Black households had a median of $44,900. Hispanic households had a median of $61,600. These disparities reflect historical differences in homeownership, inheritance, and access to wealth-building opportunities. Education also correlates strongly: households with a college degree had a median net worth of $308,200, compared to $68,200 for households without a college degree.

Final verdict

Median net worth is the right benchmark for most people. The Federal Reserve's 2022 Survey of Consumer Finances gives us the most current authoritative data: households under 35 have a median of $39,000, rising to $409,900 at ages 65-74. These are the numbers that reflect where typical American households actually stand.

Average net worth is dramatically higher at every age group -- four to five times the median -- because a small number of extremely wealthy households pull the mean upward. Using the average as a personal benchmark makes most people feel far behind when they are near or above the typical position.

Realistic benchmarks by age:

- ✓Late 20s: positive net worth, trending upward, any student debt on a clear payoff path

- ✓Mid-30s: at or above $100,000-$135,000 (median), emergency fund in place, retirement accounts growing

- ✓Mid-40s: at or above $200,000-$250,000 (median), significant retirement savings

- ✓Mid-50s: at or above $300,000-$365,000 (median), on track for retirement income needs

- ✓Early 60s: net worth review against retirement spending requirements

The most important variable is not the current number but the direction. Net worth growing consistently over time, with debt declining and investments increasing, is the pattern that produces financial security. Many people compare their assets and liabilities using the Vortenza Net Worth Calculator before comparing themselves to age-based benchmarks. Working through the actual numbers often reveals a different picture than the intuitive sense of where someone stands.

About this guide

Published by the Vortenza Editorial Team. All net worth benchmark figures sourced from the Federal Reserve Board's 2022 Survey of Consumer Finances (SCF), published October 2023, the most current authoritative US household wealth data available. Percentile figures derived from SCF microdata analysis by DQYDJ and supplemental Federal Reserve Distributional Financial Accounts data. The 2025 SCF is underway with results expected late 2026. Racial wealth disparity data from Federal Reserve SCF 2022 tabulations.

Tools used in this guide

Net Worth Calculator

Calculate your current net worth and compare to US median benchmarks for your age group. Free.

Compound Interest Calculator

See how consistent investing builds net worth over time. Free.

Emergency Fund Calculator

Determine the right emergency fund target for your situation. Free.

Debt Snowball vs Avalanche Calculator

Plan your debt payoff strategy to grow net worth faster. Free.